Discover A Hidden Canadian Stock Positioned For The Next AI Bull Market

A Unique Opportunity in "Applied AI" And How You Can Get In Before The Institutions

The Problem With “Investing” In AI

Two months after its launch, ChatGPT reached a peak of 100 million users.

Since then, investors have been clamoring for a way to invest and profit from the AI space.

It’s been tough. The big plays are all private with massive valuations, and the current public offerings that are “pure” AI plays leave a LOT to be desired.

Instead, the primary winners in the AI space have been “proxy” plays, where a company is a service provider to all the AI firms.

Like NVDA.

They are (currently) top dog in the semiconductor space, selling H100s to the big AI companies as fast as they can make them.

Yet in terms of “AI Stocks,” there’s not much out there.

I’ve found one. An absolute gem of a company that is tucked away in a smaller market. And I can tell you that there are institutions who can’t wait to buy this stock once they get the “green light.”

Better yet, this AI company could be profitable next year.

When’s the last time you heard about an AI company that wasn’t bleeding cash?

This is an incredible story with a very unique situation.

That’s why I went out and spoke with the CEO of the company.

He has much better hair than me. Kinda jealous.

I’ve provided an executive summary at the bottom of this post if you need to get the tl;dr version, yet I think you will appreciate this company more if you know how it was founded and why the company is “best in class.”

The Origin

In 2018, a company named “WELLHealth” was founded.

It trades on the TSX under stock ticker WELL.

Through strategic acquisitions, the company has grown to a valuation of around $1.15B.

It operates primary care clinics in North America, and also has a SAAS arm that allows other clinics to access their software.

That software focuses on managing clinical data through electronic medical records (EMR) processing and storage.

In other words, they have a ton of clean healthcare data.

How much do you think that data is worth?

The Spinoff

While looking for acquisitions, the team at WELL Health found a small network of clinics.

That company’s name was MCI OneHealth.

It also had a “Data Science” part of the business. The way they structured the deal was that WELL Health would absorb the clinics, and then the Data Science arm would spin out as its own company.

That is how Healwell AI (TSX:AIDX OTC:HWAIV) was created, and it sits at the forefront of the next AI bull market.

The relationship between WELL and Healwell is very close, and it gives both companies a massive advantage into 2025.

More on that in a moment, but first you’ll see where this company sits in the AI Stack.

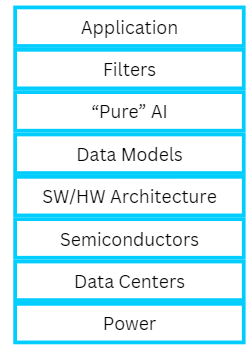

The AI Stack Profit Centers

The OSI model gives us a way to view the Internet as a series of layers, from the physical layer all the way up to what the user sees.

Each of these layers hosts multiple companies that are valued in the billions of dollars.

And each layer goes through its own bull market. In the 2000 tech bubble, the physical layer was hot, with CSCO going parabolic as they made the switches and routers.

After that collapsed, other layers would run.

You had social networks, mobile apps, API-driven SAAS companies, Content Delivery Networks, Cybersecurity…

An entire ecosystem of different technologies and companies, many of which still give investors career-making returns.

The AI Framework

… is still new.

We don’t have a full grasp on what the entire “stack” will look like, but the market has started to carve-out the “layers.”

Here’s my best guess:

The most popular layer is the semiconductor space. That means NVDA.

I’m not bearish on NVDA, just that there are other layers that haven’t seen liquidity infusions driving up prices.

The base layer for the AI stack is going to be Power, and we’ve started to see those names run.

There’s also the Pure AI layer with names like ChatGPT and Anthropic. They are still private, although the mega-cap tech firms are a way to get small exposure in the space.

The next big AI bull market is going to be in Applied AI. This is where you take an LLM and interface it with new data.

We’ve already seen one big mover in the Applied AI arms race: Palantir (PLTR)

The stock is already a 10x and probably goes much higher.

Why? Because they are positioned to be the Applied AI layer for the Defense Department.

They have an advantage because they have clean data about warfare that can be easily modeled and leveraged with the current AI technologies.

What about healthcare?

What is the value unlock for an Applied AI Healthcare company?

The Partnership Provides The Profits

When you look at AI plays, you expect them to be bleeding cash as they “grow” their way to a higher valuation.

At the time of this writing, Healwell has zero debt.

And into 2025, they are guiding for a run rate of $87mm and could end up being profitable.

WTF?

A profitable AI company?

How are they pulling this off?

It goes back to the relationship between WELL and Healwell.

WELL Health is a large shareholder in Healwell. On first pass, I viewed this as a risk, where misaligned incentives could end up hurting retail investors.

Yet after speaking with the CEOs of both companies, I realized that the partnership is the primary reason why Healwell can position itself into being best of class.

There are 3 “Profit Inflection Points” that prove it.

For each one, we will consider the difficulties faced by an AI Healthcare startup, and why the WELL-Healwell partnership allows them to bypass this.

It’s how they build out their moat, and why institutions are going to step over themselves to buy this company.

Profit Inflection #1: The Data

Imagine you want to start a healthcare AI company.

You raise some funding, hire a couple AI/ML devs, and pull the best LLMs out of Huggingface.

That’s great. You still don’t have a business.

You need the data.

Good luck.

There are ZERO companies that are willing to give that to you. This is not just valuable data— it has legal protections. Privacy regulations like HIPAA create a high barrier to entry, as hospitals and clinics view data sharing as a massive risk.

WELL Health provides Healwell with all the data they need. WELL has pioneered the use of Electronic Medical Records (EMR) and has pre-structured the data so it can be used for data science.

They’ve got a head start in the AI Arms race that is virtually impossible to replicate.

And due to the relationship with WELL, they aren’t paying out the ear for that access.

That means lower costs. And higher margins. And actual profits.

Profit Inflection #2: Diversified Revenue

Imagine you’re the struggling healthcare AI startup, and you’ve managed to secure data from a hospital network at a very high price.

Now, you’re ready to monetize.

How?

My first thought would be to sell an AI “copilot” for doctors to help them better diagnose patients.

It’s a good idea but a hard pitch. You want to go back to the same hospital you pulled data from and sell software to them?

At that point, the hospital may just consider bringing all of this “in house” or hiring out consultants.

Even if they decide to buy your product, it’s not going to be at a higher price than the cost of the data. You’re still operating at a loss, and your clients could rug-pull you at any point.

Healwell does have SAAS offerings for health care providers, and because their AI data costs are low, they are able to quickly compete and win new clients.

Yet that’s not the “big win” for Healthcare AI.

Pharma companies need patients for drug trials. Recruitment costs for these trials can be very expensive— tens of thousands of dollars per patient.

Think of the budget that these pharma companies put into trials— 30-40% of that budget is for patient recruitment alone.

Healwell helps Pharma companies find clinical trial patients. They can do it faster than most, and they are compensated well for it. The company has worked with over 250 Pharma clients, and have ongoing relationships with 6 of the big 10 pharma companies.

Here’s where they can crank up the value for pharma companies.

There are some patients that will do better during pharma trials. Before AI, that would be very difficult to pin down. But now they can find the “best in class” patients to help pharma companies get trials done with better results.

Profit Inflection #3: Capital Allocation

Our imaginary Healthcare AI startup has managed to get the data and find a few clients.

The problem is that they are having trouble with organic growth because selling to doctors and pharma is very difficult. You need a talented sales team with experience and networks.

That’s hard. Maybe you can just buy another company instead.

Problem is, you’re a Healthcare AI startup that’s bleeding cash with no data moat.

You don’t have access to any debt facilities, so you would need to do a round of equity financing. Using creative methods like earnouts would be a tough pitch for the acquiree if you don’t have a track record.

Which means finding new investors, who hopefully won’t dilute your stock too much.

That also means having the right financial partners that set it all up for you.

Again… that ain’t happening.

Remember how Healwell got started? It was a spinoff from MCI Onehealth, which was acquired by WELL.

The CEO of WELL is Hamed Shahbazi, who is also the Chairman of the Board at Healwell AI.

Before running WELL, he built TIO Networks and sold it to Paypal for about 300mm CAD.

He’s got expertise in the financial space, and it shows. WELL Health has made over 80 acquisitions. They have written down zero of these purchases, and the company has grown to a billion dollar valuation.

The WELL team has a track record of success. And Healwell has access to that success.

They share the same CorpDev team. That means the networks and capital that WELL has built over the past 6 years can be used to grow Healwell.

They’ve been busy.

They acquired Verosource, a healthcare data management company

They acquired BioPharma Services, a Contract Research Organization (CRO) that works with Pharma companies.

They acquired Pentavere, another AI company for healthcare data

They acquired Intrahealth, a company focused on electronic health records

The company is buying earnings, with all of these deals being accretive to the valuation of Healwell.

These three profit inflections are why the company is set to have a revenue run rate of $80mm+, and expected to be profitable on an adjusted EBITDA basis.

Profitability matters. It affords them more paths to growth. They can now take their existing assets and grow them organically, and use their market position to continue to acquire companies through growth.

And the pedigree from both WELL and Healwell mean they get access to the best banking partners.

Those banking partners are going to allow a massive value unlock next year.

The Liquidity Event You Need to Front-Run

There is a massive distance between a company and its stock. You can have the most well run operation and amazing numbers, but if you don’t have access to liquidity then the stock will continue to trade poorly.

Healwell is currently listed on the Toronto Stock Exchange under the ticker AIDX. It’s currently trading 500,000 shares a day on a stock price of around $2.

The stock also trades over the counter with ticker HWAIF with a daily volume around 70k shares.

The liquidity sucks on this stock. And low liquidity means higher volatility. It’s how the stock can drop 50% off its highs.

The stock needs to do well, because that signalling can get them access to better deals. It’s how reflexivity works.

That means, at some point, they will need to list on U.S. exchanges. Probably the Nasdaq. Because right now, institutional capital is very limited with respect to getting access to this name.

But they know about it. The barbarians are at the gate, and they want a piece.

This is where their banking partnerships come back into play. Normally, a TSX/OTC stock is going be involved with mid-tier banking partners, because that’s who you have to work with.

The unique relationship with WELL changes this relationship. They are working with a Tier 1 bank, and although they haven’t announced anything official, I think they will make a push to list on the Nasdaq in 2025.

At the beginning of this post, I revealed how financial capital is aggressively searching for a home in AI-related companies, but there are not many out there.

If Healwell hits the Nazz, momentum will follow as investors will uncover the narrative that I’ve already revealed to you.

If you have the risk profile for it, then front-running this liquidity event is a no-brainer. The company has actual revenue, organic and acquisitive growth, and no debt.

It won’t stay under the radar for much longer.

The Capital Stars Are Aligning… But It’s A Small Window

You don’t come across a setup like this very often.

There’s a clear narrative tailwind with AI.

The company is in a solid financial position.

It has a liquidity event due in 2025.

For US-based investors, the best way to get access to this stock is OTC under the ticker HWAIF.

If you think this company fits your risk profile, talk to your financial advisor.

Executive Summary

Company Name: Healwell AI

Stock Ticker: AIDX (TSX) | HWAIF (OTC)

The strategic relationship between WELL Health and Healwell AI has allowed Healwell to quickly grow their revenue and are now positioned to be the “best in class” company in the Applied AI space. If a liquidity event happens next year, early investors are positioned for solid rewards.Disclaimers and Disclosures

This post is not a recommendation to buy or sell any securities, I’m providing you with a narrative and a jumping off point to do more research. I’m not your broker or financial advisor, and you should talk to them before making any decisions.

I didn’t receive any compensation to write this analysis.

HOWEVER!

The company did fly me out to Scottsdale to talk with leadership. I got a hotel room, some food, and a round of golf.

That could always bias my analysis, so I encourage you to do your own research. I’m certain that if you do, you will be as excited as I am.