I Discovered The Ultimate Contrarian Bet In North Colorado

Fracking, financing, and finding a bottom in the most overlooked sector in the stock market.

Earlier this year, I had the opportunity to tour a few oil sites out in Colorado. The wells are owned by Prairie Operating (PROP), which is a new oil rollup play in the Denver-Julesberg (DJ) basin.

I’ve been speaking with company leadership over the past few years about their project, and the timing appears to set up investors for an upside play in a space that is not the radar of Wall Street.

I’m going to lay out a “deep value small cap oil” bet in Prairie Operating that I view as a special situation in the markets.

You’ll learn about the major market dislocations that are taking place in the oil markets, how Prairie is taking a big bet in the space, and what they need to do in order to get it to pay off.

“Turning Chicken Shit Into Chicken Salad”

That’s what the CEO told me as we were driving out to Northern Colorado. The DJ basin is not known for the highest quality oil, and that trend is continuing.

The oil is shifting towards heavier hydrocarbons, which affects the output yield. There’s also a higher gas-to-oil ratio that can hurt profitability unless NatGas prices have skyrocketed.

Yet the CEO, Ed Kovalik, is bullish on the region. His team has run the numbers, and looked at the deals in the space, and are now making a very concentrated bet to become the new “rollup” play in the DJ oilfields.

The timing is as good as it’s going to get.

Take The Time Machine Back to 2014

In the aftermath of the Great Financial Crisis, macro investors were positioning for the inevitable inflation from the QE money bomb.

It never showed up.

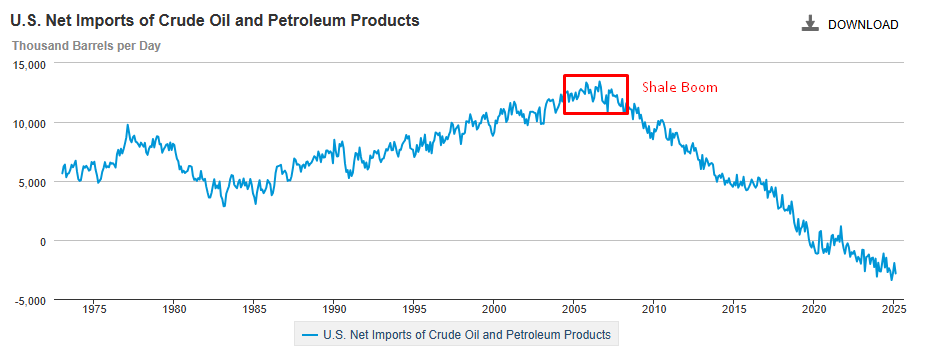

The fracking revolution was taking hold in the United States. This drove oil prices lower and has allowed the U.S. to become a net exporter of energy:

This changed the economic math around the fiscal and monetary situation of the United States, and it was a key drive in staving off any inflationary pressures that could have hit in the early 2010s.

The Shale boom ran hot, until it didn’t.

In 2014 there was a nasty unwind in the energy markets due to the overbuild in the shale markets.

Multiple Oil MLPs went under, and there was a fire sale on oil assets.

This is where private equity stepped in. They were able to scoop up land, permits, and equipment on the cheap and continue to operate them from a position of strength.

That was a little over 10 years ago. That’s not just a big round number… that’s the normal timeframe for a PE fund.

Here’s the opportunity: the private equity funds that bought oil assets a decade ago are looking to get liquid and divest out of the DJ basin.

(So are public companies like Civitas and Occidental.)

This is a major market inefficiency that Prairie Operating is looking to exploit.

Back in March they completed a $600mm acquisition from Bayswater, a private E&P company. They immediately started drilling on one site, and started a fracking operation on the other site.

These aren’t speculative wells, they know where the oil is, and if they can produce at the rate they claim, then their acquisition was a screaming deal.

If This Is Such a Great Play, Why Does The Stock Suck?

There’s a famous quote from Benjamin Graham:

“In the short run, the market is a voting machine but in the long run it is a weighing machine.”

Here’s some advice: if your financial advisor ever starts a meeting with this line, that means you’re about to get some really bad news about your investments.

When you’re looking to invest in a company, you must understand that the company and its stock are two separate things. The stock is the abstraction of the company’s value, set by a market that has limited liquidity.

In other words… if nobody wants to buy the stock, price goes down.

So I could try and hype up the company’s prospects more, but if institutional buyers don’t show up, then it’s not going to lead to a profitable investment in the company.

If we view this investment from an institutional lens, what do we see?

It’s an Energy Stock.

Here’s a look at the relative performance of XLE to SPY:

That’s nearly 20 years of underperformance!

It’s rough out there: the entire energy sector has a collective market capitalization that’s less than Microsoft.

It’s a Small Cap Energy Stock

Here’s the relative performance of PSCE (small cap energy) to XLE (large cap energy):

Again, for over a decade this market has been one giant value trap.

It’s a Small Cap Energy Play in The DJ Basin

I’ve mentioned the concerns about the energy blend and density changing, which is prompting Civitas and Occidental to look for sellers.

There’s also political and regulatory risk in Colorado compared to dealing with a friendlier environment like Texas.

Here’s a chart of CIVI relative to XLE to show how it hasn’t been a good bet to buy a “pure play” in the DJ basin.

It’s a Dilutive Small Cap Energy Play

I think this is the primary driver, and it’s easy to see when you look at the market cap of the stock over time:

The company made a new high in its valuation in 2025, yet the stock traded 40% under its 2024 highs at the same time:

Before the Bayswater acquisition, the company had a market cap of around $150mm.

The Bayswater deal was valued at $600mm, which included a $200mm equity raise along with a $400mm credit facility.

In this kind of market, with where interest rate sit, institutions don’t want to touch this deal. You’ve got a small company that quadrupled their size using a combination of stock and debt.

There’s little consideration if it’s a good deal— the market has been flush with “deals” that ended up diluting existing shareholders into dust.

All of these risks are “known knowns.” What would it take for institutions to start piling into the stock?

The Only Metric That Matters For The Stock’s Turnaround

The risk premium from all of these themes are baked into the stock.

Yet it’s those same risks that could cause a reverse unwind and the share price catches at least a double from these levels.

It all hinges on one thing.

Are the Bayswater assets going to pay off enough to make the deal accretive to the company relative to the debt and equity financing?

On paper, the answer looks like a “yes.” They bought the Bayswater project for an EBIDTA multiple around 2, and market rates are around 4.

Execution and results are going to be what matter here.

When I visited their drill sites, they were finishing up on new wells and starting up fracking on some other wells. That means in the next quarter or two, the company can provide updates on production and whether their purchase was a screaming deal or a flop.

If the production numbers play out, then the downside pressure from dilution risk is removed.

(That means stock go up.)

The company could then access further debt facilities to bring on more acquisitions given the market dislocations we’re seeing in the DJ basin.

From there, it is going to come down to how they best allocate capital. Are they going to kick out a cash dividend? Maybe buy back some stock? Or use their cash flow to add more assets to the company?

Those would be good problems to have, and well-timed investors could be compensated exceptionally well with those answers.

Looking to Invest? Read This First.

Prairie Operating is listed on US exchanges and trades under the ticker symbol PROP.

Consider this a “venture” level investment. It’s either a triple or it’s a zero. That can help dictate your position sizing.

If the Bayswater assets pay out, that only removes one of the risks.

Energy stocks still suck. So do small cap energy stocks. There’s a lot of macro shifts that have to happen, so you may end up “standing on your head” for a few quarters before there’s any appreciable lift in the stock. That may not be due to anything that the company has done— instead, it’s market and sector specific risk.

In front of all those risks is the special situation. Prairie is projecting adjusted EBIDTA of $350-$370MM this year.

That puts their EV/EBIDTA at about 0.5x.

CIVI has their multiple around 2x, which means if PROP’s value normalizes, share price rises 300%.

It’s just going to come down to how much oil they pull out of the ground, what price they sell it at, and the value of the deal.

Disclaimers

You know the drill— do your own research, I’m not your broker/dealer, consult your financial advisor before putting any risk in the market.

My tour of Prairie’s operations was part of an Investor Relations campaign, where they want to have people like me talk about the stock so that investors will buy it.

I did not get compensated for writing this report. But I should, it’s an absolute banger.

The company did pay for my flight and hotel out to Denver. And if you think you can get me to talk about your company in exchange for a good hotel breakfast buffet, you’re absolutely right.

Happy hunting!