Rebrands and Fried Dopamine

I've uncovered the biggest risk to the markets, and it ain't the Fed. How to trade the latest design debacle, and placing bets for the next AI wave.

The Brands Are At It, Again

Cracker Barrel (CBRL) was down as much as 14% today. It wasn’t earnings, or same store sales. It was another “millenial kitsch” rebrand.

I’ve been a “fan” of CBRL in the past. It had some incredible runs in the early 2010s, so the ticker has always stuck in my mind.

But… we’re a Waffle House family. I didn’t eat at a Cracker Barrel as an adult until just a few years ago, and I was impressed. Good food at reasonable prices, and a vibe that seemed ironic pre-2020 but now has a sincerity about it.

And they killed it. No, literally killed the brand.

It went from “messy fish camp” to “sterile millenial grey.” This isn’t going to work.

HOWEVER - this kind of story pulls a ton of volatility into the stock, and that can get some solid setups.

The stock has been dead money for years. Food inflation was a major cause of the last push down, and it did technically have a double bottom.

Maybe this bad news is what it needs. The company announced last year that their rebranding initiative was going to run $700 million. If they see the sentiment (and the stocks’ reaction) then they can reallocate that capital back to something more useful to shareholders.

Like a stock buyback.

Casual dining could make a turn soon if food deflation shows up. Eggs are (sorta) cheap again, and while beef is going parabolic, the softs have reset.

I actually think Denny’s (DENN) of all stocks could be a good bottom-fishing trade:

So don’t sleep on Cracker Barrel. Or Disney. Or Victoria’s Secret. You’d be shocked at how well these “murdered brands” trade.

The New AI Layer

Earlier this month, OpenAI announced GPT 5. It’s setting new benchmarks, showing improved reasoning, and can specialize much better than its prior versions.

The problem? Unless you’re a power user, unless you’re someone who has been working with the tech for years…

…you don’t care.

Humans are terrible at operating in an exponential environment. Our dopamine gets fried. Yeah, it was cool that we can generate images from a prompt, but people don’t know the incremental difference anymore.

I’m sorry to say, that investors are people too.

If they start having a hangover from all of the AI breakthroughs, it’s going to be reflected in price action.

The Mag7 are all tech momentum stocks. I don’t care that they’re trading at a $4.5T valuation, the owners of these names are a bunch of panicky sheep. They’re not “investing” for the dividend yield or because it’s trading at fair value.

And if there were a statistically normal pullback in these names, then those investors would start hunting for a narrative. And all it would take is a small whiff of bearish headline and they’ll glom onto it like a bunch of panicky idiots.

What kind of headline would it take? I don’t know, maybe something like Meta pausing AI hiring:

This is the biggest risk the market faces. It’s not the Fed, it’s not corporate earnings, it’s positioning and the psychology of those investors. That’s what has me spooked

There are going to be other AI plays. I’ve talked about solar and the power demands, which are starting to show up in utilities. There’s also the agentic MPC play, which I’ll need to write a deep dive on as it’s got monster upside.

There’s a Better Edge In These Names.

But you also have applied AI. Companies that have added a layer onto existing software to increase the value of their offerings.

Roblox (RBLX) is a great example of a run. It’s gaming engine is easy pickings for AI tools and it was accretive to their ecosystem.

I did get bearish on this stock, suggesting the Oct $110 puts at 2.90 for Convex Spaces Clients, which are currently trading for $6.70 and I think it could roll more.

Yet there’s names that haven’t seen the capital rotation for the applied AI trade.

Tempus (TEM) is one that has been stuck sub $75 since its IPO and could be ready to go:

Convex Spaces Clients got this setup on August 12th, with the Oct $80 calls at 4 bucks and are currently up at a double for $8.

There’s one more that hasn’t had it’s moment yet, but it’s setting up.

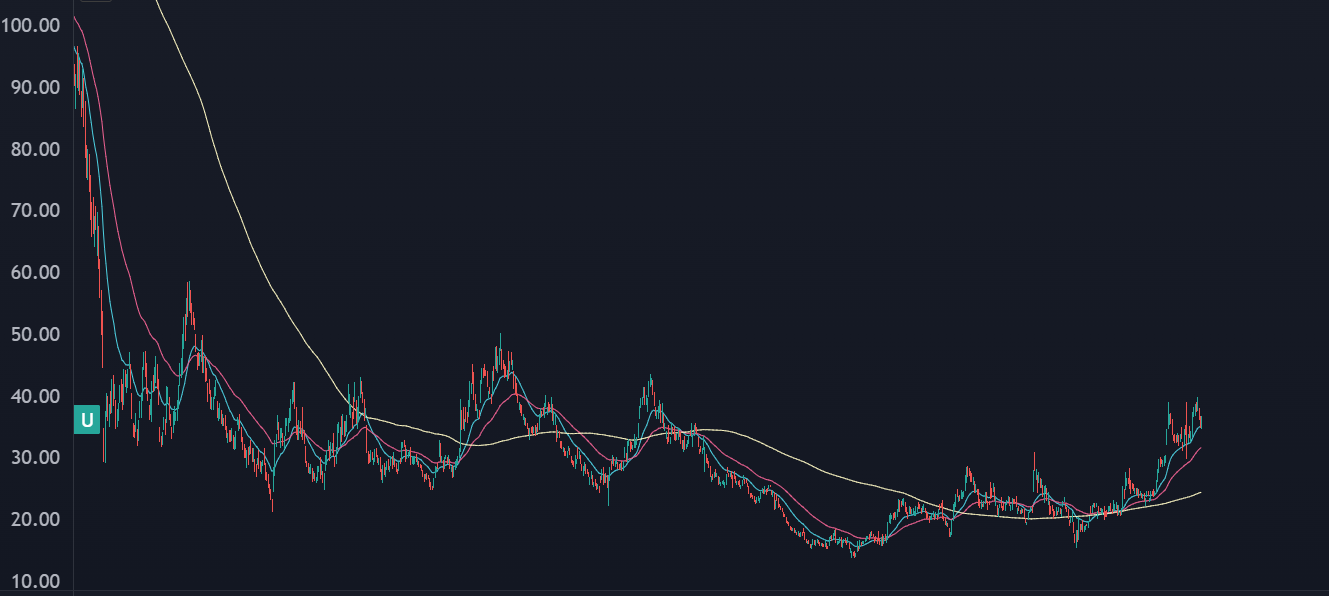

Unity (U):

Multi year base, the company had big issues in 2022 with pricing problems and the usual tech wreck risks. They recently released UnityAI in beta, which is a gaming development engine.

This could be a Roblox-like setup, where the accretive value add onto their existing game development layer unlocks a ton of value in the stock.

Next up, today’s setups for Convex Spaces Clients. One China play where you don’t have a choice but to hold your nose and buy. One “AI Layer” trade that is now proven and setup for continuation. And a PMCC setup that can offer some solid yield.

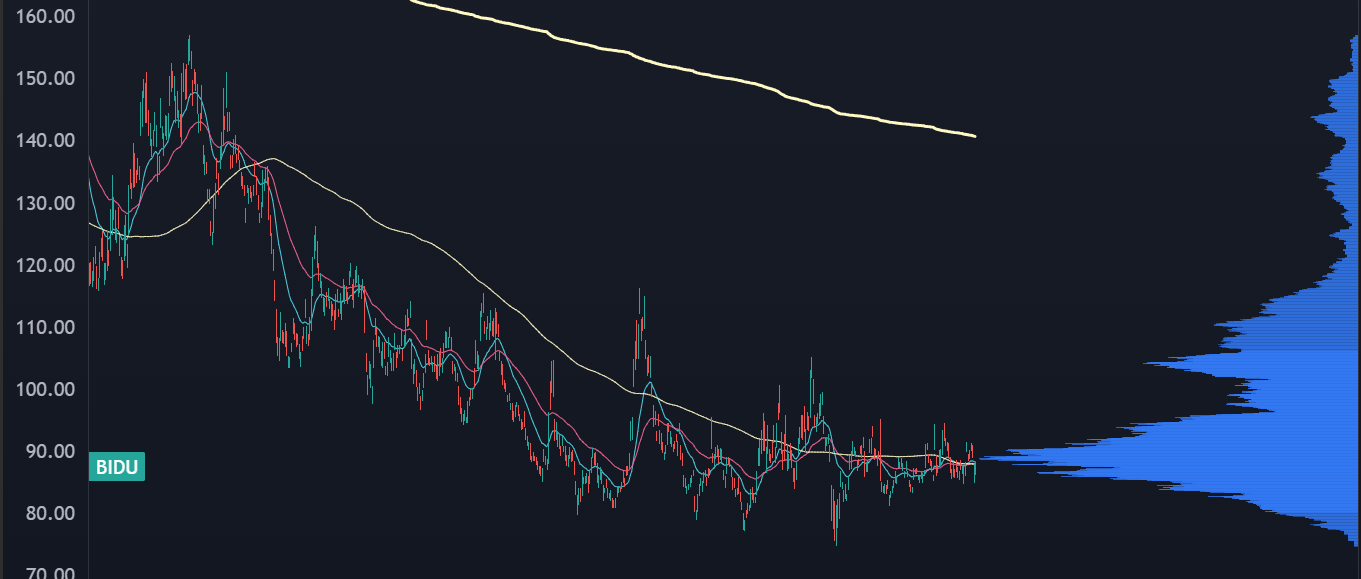

This China Play Has Cheap Enough Options To Set and Forget

There’s been a massive volume buildout in BIDU, and the stock hasn’t gone anywhere with a decent amount of compression and lower price ranges, which signals improved liquidity… and that usually signals higher prices.

The Jan $120 Calls (ref: 1.80) are sitting at a .16 delta and that’s cheap relative to what the stock can do. I think it’s got a fast date with $100 which puts the calls over a double; you can sell half and let the rest ride.

PMCC In LULU

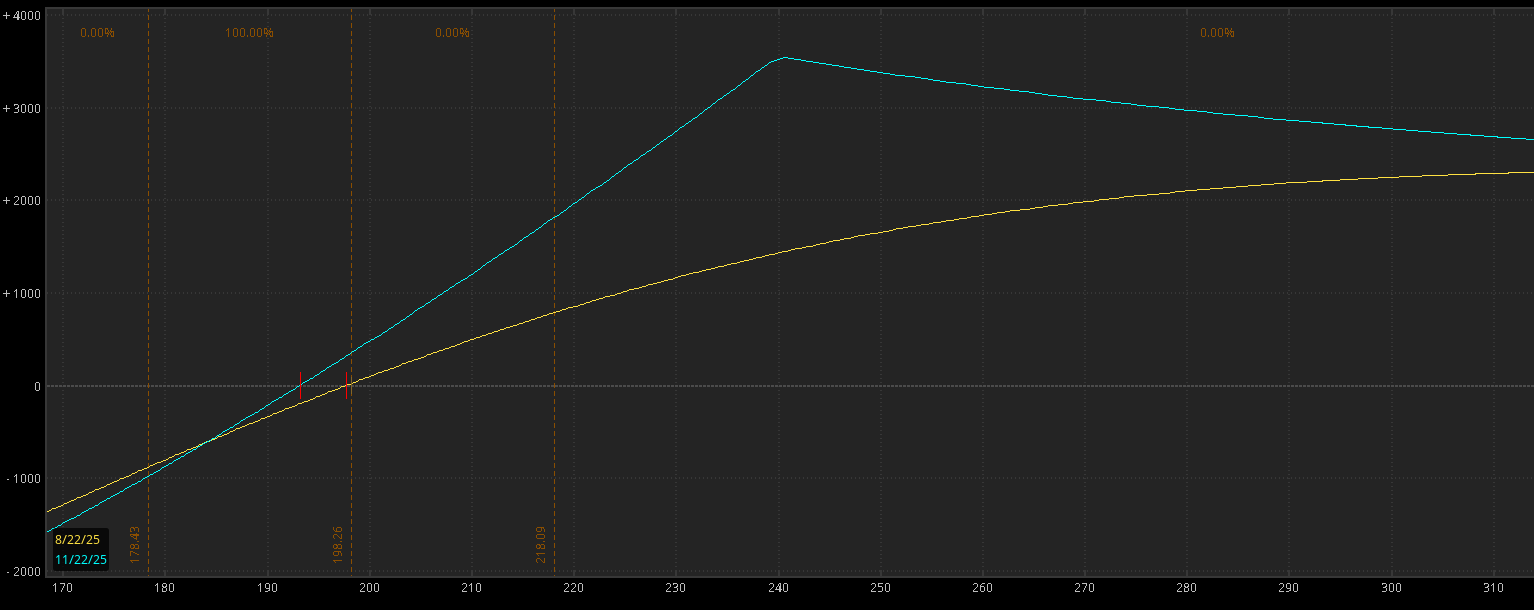

LULU is pretty oversold, and is coming into the last liquidity zone prior to the COVID lows. I think we’re close to a bottom but there’s room another $20 lower.

I think you can start scaling into a “poor mans covered call,” buying some LEAP options and selling some Nov options against it.

Buy to Open LULU 18Dec26 $180 call for $57

Sell to Open LULU 21Nov25 $239 Call for 8.10

This is a longer term bet, with the intention of selling calls against the LEAP option for the next 6-9 months.

I’d really look into scaling this, if I’m early and this pulls back, then you can use some capital to roll the long calls down, or just adding another round of PMCC’s at lower strikes.

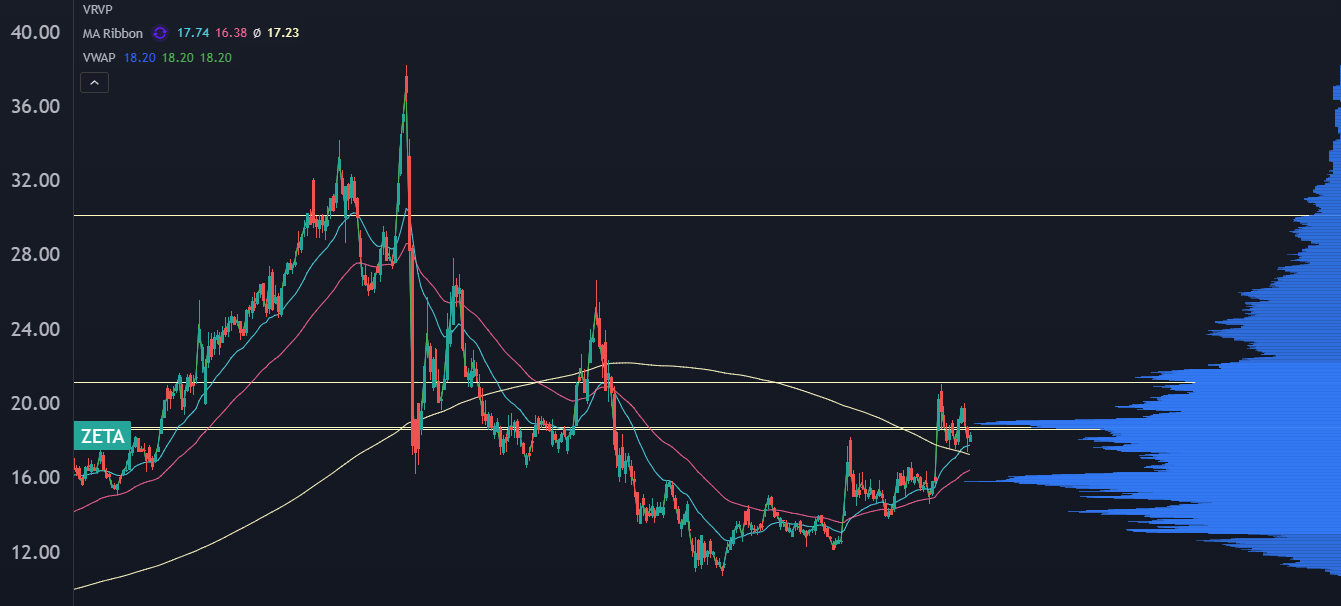

ZETA “AI Narrative” Con’t Long

This is a post earnings continuation trade for an Enterprise SAAS company that has proven its new AI layer.

The stock crash last year was due to allegations from a short seller firm. The company hired an auditor to run a forensic review and they didn’t find anything. The most recent earnings report was solid:

beat earnings

raised guidance

positive vibes from AI marketing platform

That’s enough to attract the eyeballs of investors looking for the next PLTR. It won’t be— I’m looking for $30 not $300.

The stock has been rangebound since that earnings report, and the most recent undercut held.

The Dec 22.5/30 Bull Call Spread (ref: 0.84) is a solid risk/reward into an end of year squeeze.